Key updates in the proposed revision

What has happened? The European Financial Reporting Advisory Group (EFRAG) published a draft of the revised European Sustainability Reporting Standards (ESRS) on 31 July 2025. The draft introduces a range of changes aimed at reducing the reporting burden. Below is a summary of the most significant proposed updates (click each point to expand and read more).

FEWER DATAPOINTS

• More than 55% of mandatory datapoints have been removed

• Most voluntary datapoints are deleted

SIMPLER STRUCTURE AND MORE FLEXIBILITY

• Mandatory disclosures clearly gathered

• Less repetition across the report

• More flexibility in presenting the sustainability statement

CLEARER AND MORE PRAGMATIC DMA

• Business model-driven approach

• Top-down process encouraged

• Two options for disclosing financial effects

STREAMLINED CROSS-CUTTING STANDARDS

• Disclosures on policies, actions, metrics, and targets simplified

• Some narrative requirements reduced

CONDENSED TOPICAL STANDARDS

• Fewer required disclosures across topics

• New guidance for specific metric calculations

INCREASED INTEROPERABILITY WITH IFRS

• Most changes aim to align with IFRS (International Financial Reporting Standards)

• References to ISSB and GRI sector standards included

TARGETED RELIEFS INTRODUCED

Reliefs on: reporting scope (e.g., acquisitions/disposals), evidence for DMA, financial effects, and certain metrics and estimations

EFRAG has published amendment logs for each standard, making it easier to navigate the proposed changes.

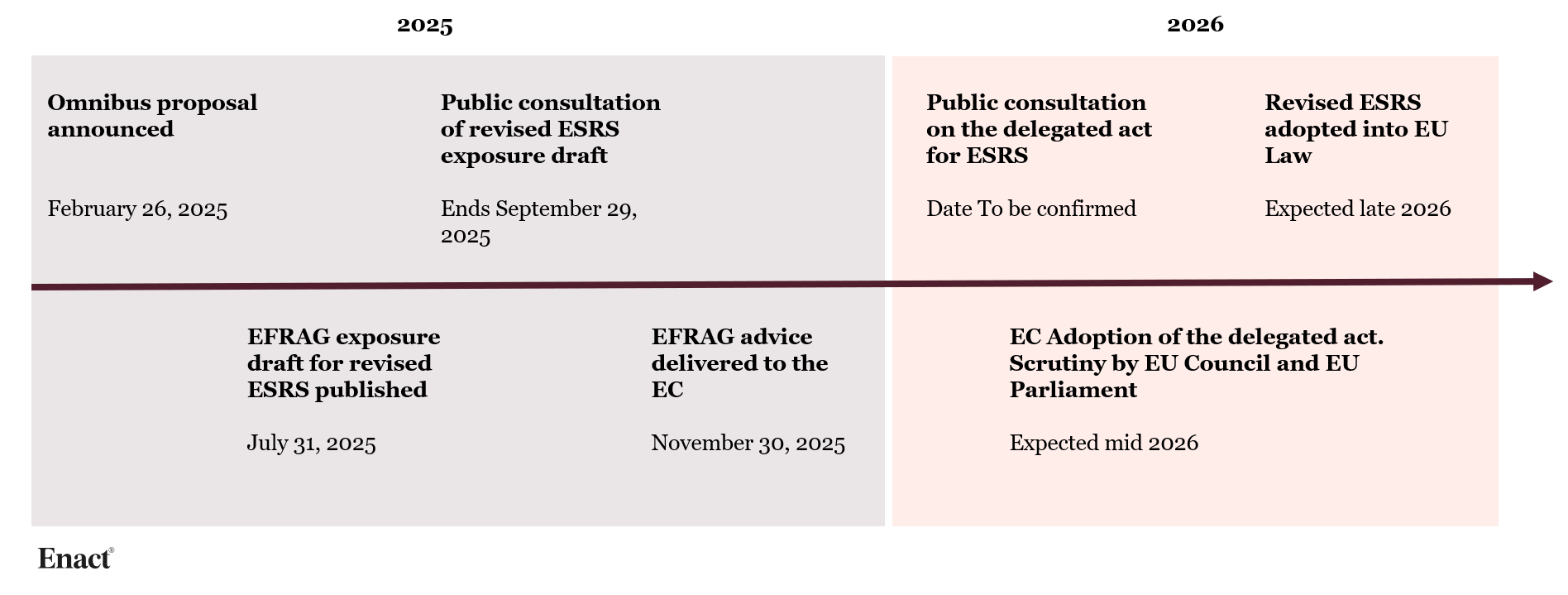

Timeline revised ESRS

The revised ESRS will likely not be adopted until mid-2026, but key milestones in the consultation and adoption process are already underway. The timeline below outlines what to expect next.

What companies should do now

If you have already published your first ESRS-aligned report:

You’re ahead of the game! With the final revised standards unlikely to be adopted until 2026, you’ll be reporting under the current ESRS for FY 2025. Rather than investing heavily in reworking your existing report, channel your energy into strengthening your due diligence processes and be ready to excel when the updates arrive.

If you have a two-year delay:

Start your Double Materiality Assessment now, using the draft revised ESRS as a reference. This will allow you to identify data needs, address critical gaps, and align sustainability with your business strategy ahead of the FY 2027 deadline. Aligning your report to ESRS is a journey – and launching a pilot report that strives to meet the amended requirements is the perfect first step.

If you have already completed your Double Materiality Assessment:

Conducting a gap analysis is a key starting point. Focus initially on E1 (Climate), S1 (Own Workforce), and G1 (Business Conduct) which are the areas where early adopters have concentrated their efforts. This approach helps you identify gaps and build solid progress without overcomplicating early reporting. Prioritize mandatory quantitative disclosures to keep momentum, then apply the same focus to other obvious material topics.

If you haven’t completed your Double Materiality Assessment:

Even if you’re not required by regulation, a DMA helps you focus on the issues that matter most to your business and stakeholders. It ensures your strategy and reporting meet investor, customer, and employee expectations, while uncovering risks and opportunities that build resilience and trust.

Regardless of your size or maturity level:

- Look past compliance: what are your stakeholders’ expectations on your non-financial information?

- Level up the quality of your sustainability data

- Strengthen internal processes — policies, actions, targets, and metrics for material topics

- Stay ahead with the latest regulatory updates

- Get inspiration and learn from Wave 1 ESRS reports

How we support your CSRD journey

At Enact, we work with organisations to make sustainability reporting both compliant and genuinely value-adding — starting with grounded materiality assessments and continuing through to action and measurable results.

Our work enables CSRD disclosures that:

- Capture your most material impacts, risks, and opportunities

- Meet regulatory requirements

- Deliver insight that informs strategic decisions and engages stakeholders

- Reinforce governance, improve performance, and support long-term value creation

Our team combines deep expertise across climate, human rights, and value chains with hands-on implementation experience across sectors.

From identifying what matters, to integrating it into business practice, we translate CSRD requirements into practical impact and strategic clarity.

Putting the ESRS in context

What the ESRS are and what they do

- The European Sustainability Reporting Standards (ESRS) underpin reporting requirements under EU’s Corporate Sustainability Reporting Directive (CSRD), translating legal requirements into a methodology for disclosing sustainability information.

- They include:

• 2 cross-cutting standards (ESRS 1 & 2)

• 10 topical standards: Environmental (E1–E5), Social (S1–S4), and Governance (G1) - Topical standards and their respective datapoints are mandatory only when they are material, as defined by a Double Materiality Assessment (DMA), which considers:

• An organisation’s impacts on people and the environment

• The financial effect of sustainability matters on the company

Political and regulatory context

- On 31 July 2025, the European Financial Reporting Advisory Group (EFRAG) published the draft of the revised European Sustainability Reporting Standards (ESRS), following its June 2025 Progress Report.

- The revisions aim to simplify the standards, reduce complexity, improve usability and decrease administrative burden for companies. They are part of the EU Omnibus Simplification Package announced in February 2025, which committed to streamlining the ESRS.

- While the ‘stop the clock’ amendment has delayed reporting for wave 2 and wave 3 companies, proposals on scope and disclosure requirements remain on the table.

- Uncertainty remains with regards to which companies will ultimately be in scope of CSRD. The initial Omnibus proposal from February 2025 suggested the threshold to be drawn to companies with over 1,000 employees and either a net turnover over EUR 50 million or a balance sheet of EUR 25 million or more.

Public consultation and next steps

- The public consultation is open until 29 September 2025.

- EFRAG will host outreach events in September and October to gather stakeholder feedback.

- After the consultation closes, EFRAG will use the input to prepare its final technical advice to the European Commission by 30 November 2025.

- While the standards may still evolve, this revision clearly signals EFRAG’s direction of travel.

- Take the opportunity to influence the future of sustainability reporting by participating in the consultation: Public consultation survey

Contact

Want to know more or ready to make the ESRS work for your organisation? Get in touch with us below.

Kerstin Pettersson, Head of Enact Sweden, kerstin.pettersson@enact.se

Sofia Svingby, Senior Advisor Enact Group, sofia.svingby@enact.se